Banking reform gets 3 yes, 2 no votes from OK delegation in Congress

Note: Before we start this post, an update on Green Country Monitor. We’re two subscribers away from 100, an important early milestone. Doesn’t seem like much. But it is if you’re doing digital journalism that’s really narrowly focused on something like cannabis policy and business news from Oklahoma. I’ve decided to ditch the newsletter format. It makes more sense to email the posts out as I complete them. So that means more emails from GCM in the future. But I’m just starting to get good at reporting on cannabis, so stay with me. You’ll like it. We’ll have fun. The newsletter format works in a lot of capacities (like, for example, cultivator-to-dispensary, or B2B, marketing). But the Substack publishing platform I’m using lends itself a lot better to the journalism distribution method I’ll be using going forward. -G.W. Schulz

Our long national nightmare in cannabis of using literally dirty money for transactions may soon be coming to an end. The only people in Oklahoma cannabis perhaps not thrilled to see this nightmare’s conclusion are dispensary operators getting a cut of the ATM fees.

Consumers today can buy virtually anything with ease from their phones and have it delivered anywhere. The celebrity Kylie Jenner reportedly used the delivery app Postmates more than 180 times over 12 months, including for a single carrot on one occasion.

Yet cannabis operators and consumers are still inexplicably forced to handle cash that travels a long journey through general commerce as it picks up COVID and poo bacteria along the way.

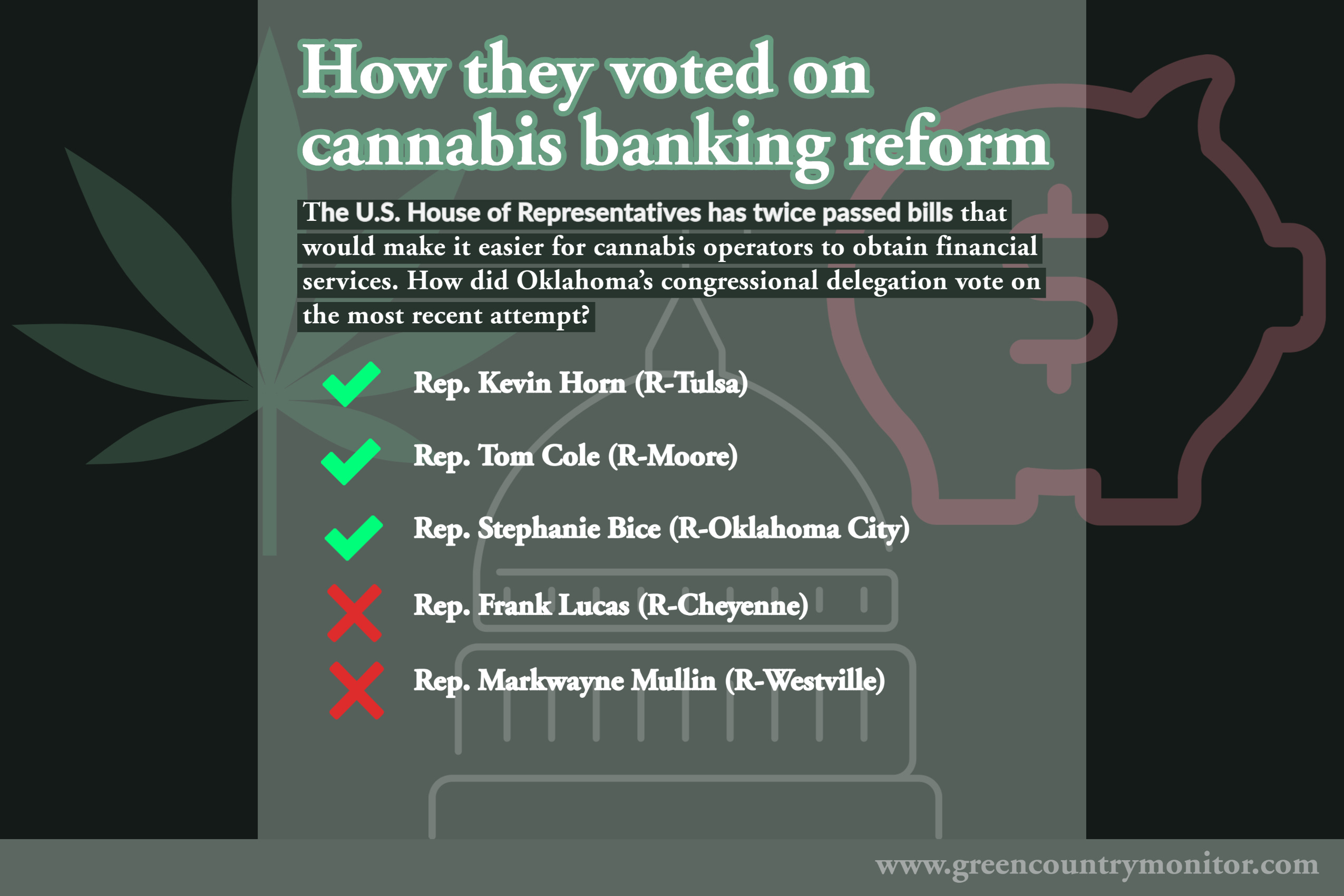

That could change with the SAFE Banking Act passed by the U.S. House in late April. The bill is showing signs it could pass the Senate, too, where it’s stalled in the past. More than 100 House Republicans backed the most recent version, including three from the Sooner State.

Oklahoma’s cannabis industry arguably has more at stake with the outcome of this bill than any other state in the nation. Mature markets with greater populations in Colorado, California, and Washington State certainly generate more in sales than humble Oklahoma.

But we have 367,000 patients in a state of fewer than four million people. We have more dispensary licensees than any state in the nation at over 2,200. Combined with cultivators and processors, we top 10,000 cannabis businesses who have a major stake in the SAFE Banking Act.

Not to mention, each of those cannabis operators has an untold number more people as workers, vendors, and investors all also with an interest in the bill.

The SAFE Banking Act generally seeks to stop federal financial regulators from penalizing banks when they conduct transactions with legitimate cannabis businesses. Banks would no longer have to worry about running afoul of anti-money laundering laws even though cannabis is still federally prohibited.

As long as that fear of prosecution exists, most banks will deny you access to financial services that would make it easier and speedier for you to buy and sell cannabis and cannabis products, pay your taxes, conduct deposits, and compensate workers. While cannabis is a booming business in Oklahoma, it’s still a fraction of the size of the state’s legacy industries. Cannabis simply isn’t worth the risk for most banks right now.

A small number of regional banks and credit unions can legally service cannabis businesses by meeting tough reporting requirements. Some of them exist here in Oklahoma, but they’re few in number. One such institution, Encentus Federal Credit Union, even ceased its Oklahoma cannabis services in 2019 after deciding it was simply too burdensome. Said one expert to the Tulsa World:

“Unfortunately, it’s not uncommon to hear of a bank or credit union that has to sever its ties with the cannabis industry. Banking cannabis properly is labor intensive, and the cost of compliance can be prohibitively high without the right tools.”

The total number of financial institutions nationally that are eligible to do business with cannabis is a mere sliver of the larger banking industry and has actually dropped since 2019. This even as states have rapidly moved toward cannabis reform. Where banks do offer such services to cannabis, you’ll likely pay much more in fees for the privilege of being banked than a traditional business.

Democratic lawmakers in Washington have filed bills attempting to end these restrictions on banks since all the way back in 2013. A version eventually became known as the SAFE Banking Act, which passed the House for the first time in 2019. Also passed by the House that year was a historic but symbolic bill that would have entirely legalized cannabis at the federal level.

Both were doomed in the Senate, however, where Republicans remained in control at the time.

Oklahoma Republicans Markwayne Mullin (Westville) and Frank Lucas (Cheyenne) have opposed both versions of the SAFE Banking Act in 2019 and now this year. Republicans Tom Cole (Moore) and Kevin Horn (Tulsa) joined former Democrat Kendra Horn in supporting the 2019 bill.

Kendra Horn was the only member of Oklahoma’s congressional delegation who supported the historic vote for legalization. She was defeated after one term following a tough, partisan battle with Republican Stephanie Bice in the November election, who supports the SAFE Banking Act.

Tom Cole says that even though he has supported both versions of the SAFE Banking Act, he continues to oppose cannabis legalization and efforts to allow adult-use. He told the Oklahoman in late April:

“Whether I agree with this new industry or not, its very existence requires a legal framework for banking, business operations, and law enforcement. The SAFE Banking Act provides financial institutions and law enforcement with the tools needed to ensure the medical marijuana industry operates safely and lawfully.”

With Democrats in control of the Senate and a corresponding bill there, the SAFE Banking Act seems to have a better chance at the moment of passing in 2021 than more comprehensive attempts at cannabis reform.

As for Oklahoma’s two senators, Republicans James Lankford and Jim Inhofe, they’ve both said they oppose the SAFE Banking Act on the grounds that cannabis remains federally prohibited. That’s according to the Oklahoma Bankers Association, which supports the SAFE Banking Act and has spoken with the senators about it.

In the meantime, as I mentioned above, there are still banking options available to cannabis in Oklahoma. Here are the three I’m aware of:

Direct number for cannabis banking: 405-260-2265

Offices in Guthrie, Norman, Mulhall, Edmond

Site for cannabis banking: osbbank.com/cannabis-banking

Bonus: They formally call it “cannabis” instead of “marijuana.” I like them already.

Indirect number for cannabis banking: 918-488-0788

Offices in Tulsa, Nowata, Oklahoma City, Bartlesville, and Springfield

Site for cannabis banking: I don’t recall them ever having a special page for it.

Ask for Director of Special Programs Keri Cain, according to this interview (I did a little more sleuthing, i.e. found her on LinkedIn, to confirm she works at their Tulsa branch)

Indirect number for cannabis banking: 405-286-5700

Offices in Oklahoma City and Norman

Site for cannabis banking: I also don’t recall them ever having a special page for it.

I’m not certain of the contact for cannabis banking at Valliance. But if I had to guess, it’d be their executive vice president and chief operating officer in Oklahoma City, Alisha Wade, who’s been really public about Valliance trying to service the cannabis industry.

Listening to: Bad Religion “Generator” Reply with an email or sign up to receive alerts. Follow Green Country Monitor on Twitter, Facebook, LinkedIn, and Instagram. If you appreciate this work, consider leaving a tip.